BCS Stories

Netflix–WBD deal to test JioStar’s OTT dominance in India

Netflix’s proposed 83‑billion‑dollar takeover of Warner Bros Discovery has the potential to consolidate power at the top end of India’s 38,000‑crore‑rupee OTT market in FY25, without fundamentally altering its mass‑market structure. The combined entity would control one of the richest Hollywood catalogues available, bringing HBO, DC, Warner Bros films and long‑tail TV hits under the same roof as Netflix’s originals, and positioning Netflix as the default destination for global, prestige entertainment in India’s metros and Connected‑TV homes.

For JioStar, the impact is more reputational than financial. Its core economics are driven by Indian sports rights, especially cricket, along with telco bundles and Hindi/regional entertainment rather than Hollywood dramas or English‑language series. That means the direct revenue hit from not hosting Warner/HBO‑style content is limited, but its standing in the premium English segment weakens as high‑ARPU urban audiences are nudged to see Netflix as the “must‑have” global IP hub while treating JioStar primarily as the home of sports and Indian mass content. In such a scenario, Netflix gains leverage to carefully test higher ARPUs, particularly on Connected‑TV households, whereas JioStar is unlikely to slash prices simply to offset the loss of a single studio and will instead double down on cricket, league properties and bundled Jio mobile and fibre plans.

The sharper pressure is likely to be felt by mid‑tier and regional streamers that have so far relied on a patchwork of licensed Hollywood titles plus modest local originals. Once Netflix secures long‑term control over Warner Bros Discovery IP, competing on sheer library size becomes almost impossible for these platforms, especially in English and global content. This will force regional players to rethink their positioning, shifting decisively toward language‑first originals, hyperlocal storytelling, sachet and micro‑packs, and deeper telco or device partnerships to stay relevant. Industry executives argue that Indian platforms will increasingly have to compete on identity and cultural resonance rather than catalogue scale.

Structurally, this accelerates a two‑pillar market architecture that was already taking shape. On one side sits Netflix, with Hollywood prestige, global franchises and a strong pull among affluent, urban and Connected‑TV viewers; on the other sits JioStar, anchoring sports, Hindi GEC, movies and regional mass entertainment, underpinned by the Jio ecosystem. Instead of a single winner‑takes‑all platform, Indian households are likely to normalise multi‑subscription behaviour, typically retaining JioStar for cricket and Indian programming, Netflix for high‑end global content, and then selectively adding or dropping smaller regional apps around that core depending on language preference, price and promotional bundles. In that sense, the deal reshapes power at the top of the pyramid while sharpening, rather than erasing, the contrast between global IP‑driven players and those betting their future on Indian storytelling.

Industry at an inflection point

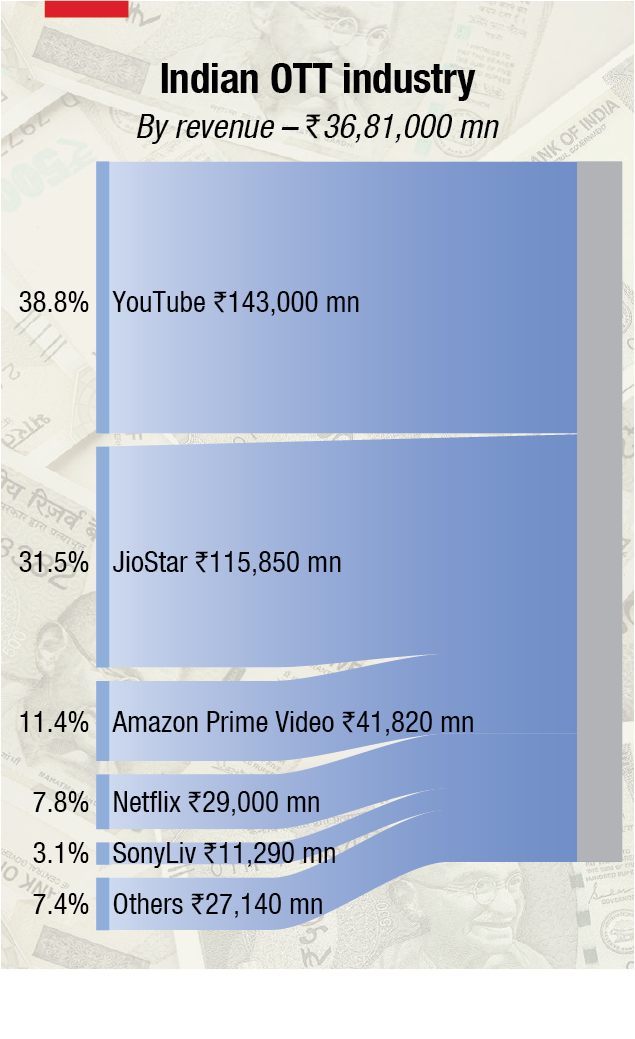

India’s OTT industry in 2025 sits at a delicate inflection point: growth is still robust, but the narrative has shifted from land‑grab to discipline in technology, monetisation and regulation. Annual OTT video revenues are estimated at about 37,940 crore rupees in FY25, with forecasts of mid‑teens CAGR over the next decade, signalling a market that is maturing rather than slowing. Consumption is deeply embedded in daily life, but paid subscription growth has flattened, pushing platforms to rethink pricing, packaging and content bets as AVOD and “free” streaming models dominate reach and revenue momentum.

Several technology currents are reshaping how Indian OTT platforms are built, discovered and monetised. AI‑driven personalisation has moved from basic recommendation rows to full‑funnel decisioning, spanning audience segmentation, churn prediction, thumbnail testing and even script green‑lighting based on likely regional resonance. Automated localisation—AI dubbing, speech‑to‑text subtitles and cross‑language recommendations—is making it viable to take a single IP across multiple Indian languages at a fraction of the older cost and time. The rollout of 5G and better 4G is enabling higher‑bitrate streaming, low‑latency sports and experimentation with 4K, multi‑camera feeds and interactive overlays, even if mass adoption is still nascent. Meanwhile, Connected TV is turning living rooms into digital ad surfaces with addressable targeting and near‑TV CPMs, giving platforms a rare mix of large‑screen impact and measurable performance.

Hard constraints—Attention, economics and trust

Beneath the surface optimism sit hard constraints around attention, economics and trust. Content costs still account for as much as 60–70 percent of platform expenditure in India even as subscription fatigue and cut‑throat pricing cap ARPUs, leaving a long tail of services struggling for visibility and sustained engagement. Discovery has become a bottleneck, with more than 40 OTT services jostling alongside YouTube and short‑video apps, driving users toward familiar brands and franchises and forcing smaller platforms into a cycle of discounting, telco bundles and loss‑leader shows. Trust is an additional flashpoint, as complaints around explicit or “obscene” content have triggered political scrutiny, public backlash and calls for tighter control, even as piracy, credential sharing and illegal IPTV erode monetisation.

Regulation, once background noise, is now a central force in this second act of streaming. OTT platforms currently operate under the Information Technology (Intermediary Guidelines and Digital Media Ethics Code) Rules, 2021, which mandate age classification, parental locks, a three‑tier grievance system and adherence to a Code of Ethics. In February 2025, the Ministry of Information & Broadcasting issued an advisory reiterating these obligations amid rising complaints of “obscene or vulgar” content and has disabled access to several smaller erotic‑focused OTT services. In parallel, the draft Broadcasting Services (Regulation) Bill proposes to bring OTT under a unified broadcasting regime alongside TV, raising concerns about obligations such as mandatory Doordarshan carriage on registered OTT services and signalling greater convergence between broadcast, telecom and digital rules.

Redefining growth—Regional, AVOD and new formats

Even with these headwinds, the opportunity canvas remains wide, especially beyond the metros. The biggest upside lies in regional and Tier‑2/3 markets, where platforms that can authentically tell non‑metro stories in local languages stand to unlock the next wave of growth, aided by AI‑assisted script testing and data‑driven green‑lighting. Advertising‑led and hybrid models, including free ad‑supported streaming TV channels inside OTT apps, are gaining ground as a bridge for TV audiences seeking digital convenience without subscription complexity, while CTV’s share of TV‑plus‑OTT ad budgets is expected to climb into low double digits by mid‑decade. New formats such as interactive storytelling, live commerce, gamified watch‑parties and creator‑led shows offer ways to differentiate beyond scripted drama, with some platforms experimenting with commerce, community and content bundles that move them closer to entertainment “super‑app” status.

Transition from scale to sustainability

Taken together, 2025 looks like the year India’s OTT ecosystem pivots from a race for scale to a search for sustainability. The platforms most likely to endure will be those that combine deep regional and genre understanding with strong data‑technology stacks and the ability to navigate a tougher regulatory climate without losing creative edge.

Within that broader transition, the Netflix–WBD deal acts as a stress test of JioStar’s OTT dominance and a forcing function for mid‑tier Indian players to choose between being global‑IP aggregators and becoming sharply defined, identity‑first Indian brands.

India’s OTT story is entering a second act—less exuberant, more complex, but potentially far more durable for players that can adapt.