BCS’s Take

Four players, one bottleneck: Inside India’s satellite broadband approval standoff

India has decided, with considerable deliberateness, not to be rushed into the satellite broadband era. The approval process has become one of global telecom’s most consequential regulatory standoffs, and the contrast between how its four principal players are faring reveals exactly how India intends to govern infrastructure it cannot afford to get wrong.

The approval process for satellite broadband in India has become a clash between the strategic interests of some of the world’s most powerful technology companies and a government that has carefully and deliberately decided to govern this new category of infrastructure on its own terms. The players in this standoff, Starlink, Eutelsat OneWeb, Jio-SES, and Amazon Kuiper are not equally positioned. They are on different regulatory tracks, with different structural advantages, and in some cases, moving toward very different outcomes. Understanding why requires looking at each player not as a technology proposition but as a regulatory and geopolitical one.

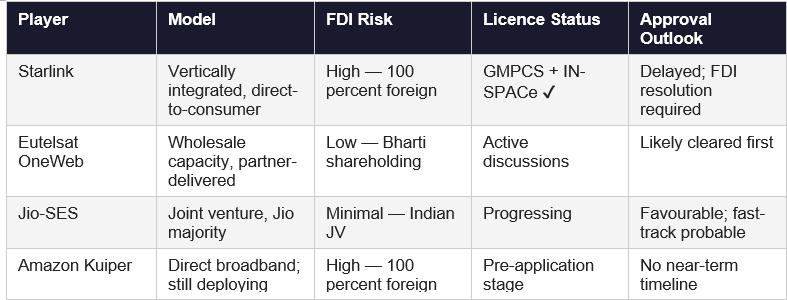

Comparative player snapshot: India satellite broadband

The regulatory architecture: Where approvals go to wait

India’s satellite broadband clearance process is not a single window. It runs through at least four distinct agencies: the Department of Telecommunications (DoT) issues GMPCS licences; the Indian National Space Promotion and Authorisation Centre (IN-SPACe) provides space activity authorisation; the Ministry of Home Affairs (MHA) weighs in on security; and TRAI advises on spectrum pricing and allocation. Any operator must satisfy all of them in an environment where agency priorities do not always align and where no inter-departmental coordination mechanism exists to resolve conflicts efficiently. The result is a process that rewards structural simplicity and punishes regulatory novelty. Starlink, as we will see, is novel in almost every dimension that matters to this government.

The foundational policy framework allows up to 100 percent FDI in satellite communications, but investments beyond 74 percent require government approval, and operators must work through Indian subsidiaries compliant with cross-holding norms under the 2023 space policy. That 74 percent threshold is not arbitrary: it is the point at which Indian regulatory and legal jurisdiction becomes materially harder to enforce. Everything happening in India’s satellite broadband approvals right now flows from that number.

Starlink: Structurally exposed, politically entangled

Starlink has, by most accounts, done the regulatory legwork. It holds a GMPCS licence. It has IN-SPACe authorisation. It operates through Starlink Satellite Communications Private Limited (SSCL), an Indian subsidiary, and has formalised commercial partnerships with Indian telecom operators. On paper, it is further along the compliance curve than any of its competitors. And yet it sits in pre-launch limbo that now stretches across multiple quarters, with no clear resolution in sight.

The core problem is ownership. Starlink is 100 percent SpaceX owned, and that structure has triggered concerns that go well beyond conventional satellite regulation. The government’s own framing is precise: “The core question being examined is what recourse India would have if a 100 percent foreign-owned operator fails to comply with local regulations despite having accepted them initially.” That question does not have a comfortable answer when the operator’s ultimate parent is a US-incorporated private company whose principal’s geopolitical footprint, including active roles in US government structures — gives any Indian security establishment legitimate pause.

Three distinct technical and political concerns have stacked on top of each other. The first is conventional: signal spillover and lawful interception capability. These are issues every satellite operator must address and that Starlink has, in principle, committed to resolving. The second is more technically novel: laser inter-satellite links (LISL). Starlink’s Gen2 satellites use LISL to route data directly between satellites in orbit, bypassing terrestrial ground stations. For Indian regulators, this creates a scenario in which user data could transit jurisdictions entirely outside India’s legal reach, a genuine gap in current international satellite governance that India is, somewhat unusually among major markets, trying to address proactively. Officials are now evaluating whether to mandate that Starlink disable or significantly restrict LISL-based routing for Indian users.

“If a company can overlook a country’s regulations because of geopolitical circumstances, what guarantees are there that it will comply elsewhere?”

The third concern is the most politically damaging: the incident involving Iran. Reports that Starlink terminals were found operating inside Iran, under US sanctions and therefore barred from Starlink access, raised a question that India’s security establishment found impossible to set aside. If SpaceX can selectively enforce its own compliance policies based on geopolitical pressure, what assurance does India have that it will not do the same in a scenario touching India’s own interests? Starlink VP Lauren Dreyer’s public pushback, asserting the company remains in active discussions, has complied with all requirements, and has built a deployment model tailored to India’s sovereignty needs, may be accurate at the technical level. It does not address the level of trust. India is not asking whether Starlink has filed the right forms. It is asking whether Starlink can be relied upon when the stakes are geopolitical.

The FDI application has been caught, sources confirm, “amid broader geopolitical and trade-related considerations.” That is diplomatic language for a negotiation that is no longer purely about telecoms. Musk’s proximity to the US administration, the broader India-US trade dynamic, and the political optics of being seen to approve a 100 percent American-owned communications infrastructure provider during a period of active geopolitical repositioning have all added layers to what should, in a simpler world, be a technical compliance review.

Eutelsat OneWeb: The structural advantage of not being Starlink

Eutelsat OneWeb’s position in India’s regulatory queue is substantially more comfortable, and its advantages are structural rather than incidental. Since merging with French satellite operator Eutelsat in 2023, OneWeb has Bharti Enterprises, parent of Bharti Airtel, as a significant shareholder. That connection is not merely financial. Sunil Mittal is among India’s most credible and politically connected industry voices on telecoms policy, and Bharti’s association with OneWeb makes the operator legible to the government in a way that a wholly foreign entity categorically is not. When regulators have questions about OneWeb’s compliance architecture, there is an Indian shareholder of consequence in the room.

The business model amplifies this advantage. Unlike Starlink’s vertically integrated direct-to-consumer approach, OneWeb operates as a wholesale satellite capacity provider. Service delivery, customer relationships, and compliance functions flow through local partners. In India, Nelco, a Tata Group subsidiary, has been the primary partner, conducting multiple security architecture demonstrations on OneWeb’s behalf with Indian agencies. From a sovereignty standpoint, this model distributes compliance accountability among Indian entities in a way that a direct-to-consumer, 100 percent foreign operator cannot. The FDI question, while present, applies less acutely. OneWeb is not asking India to trust a wholly foreign system. It is asking India to extend its existing framework of trust in Nelco and Bharti.

Sources indicate that government officials are now more inclined to clear OneWeb ahead of Starlink. This should not be misread as hostility toward Starlink, it is a rational regulatory outcome. When one operator has a simpler approval profile, it moves faster. OneWeb’s path to commercial launch, while not guaranteed, appears materially shorter than Starlink’s.

Jio-SES: The insider advantage

If OneWeb has a structural advantage, Jio-SES has something closer to structural immunity from the concerns that are slowing its competitors. The joint venture between Reliance Jio and Luxembourg-based satellite operator SES gives Jio the majority stake, making Jio-SES, for regulatory purposes, an Indian company. The FDI profile raises none of the questions that attend Starlink. The compliance obligations are anchored to an entity over which the government has exercised regulatory leverage for decades. There is no ambiguity about sovereignty when the controlling shareholder is the country’s largest telecom operator.

SES contributes its O3b mPOWER constellation to the JV, a Medium Earth Orbit (MEO) network that offers lower latency than geostationary satellites and high-capacity throughput suited to enterprise, maritime, aviation, and institutional applications. This positions Jio-SES differently in the market from Starlink’s mass-consumer aspiration: it is targeting the enterprise and government segments willing to pay premium rates for guaranteed connectivity. The competitive terrain it enters first is less contested and, critically, less sensitive from a regulatory standpoint. Backhauling connectivity to remote government installations or providing maritime connectivity to Indian shipping is a different regulatory conversation from deploying consumer terminals across rural India.

Among all players, Jio-SES faces the shortest path to clearance. Its principal challenge is not regulatory but commercial: SES’s O3b mPOWER constellation is still in the process of full deployment, and service capacity will ramp gradually. India clearance may arrive before global supply catches up.

Amazon Kuiper: The absent fourth player

Amazon Kuiper deserves mention precisely because of its absence from the current conversation. Kuiper, Amazon’s planned LEO broadband constellation, a direct competitor to Starlink, is still in its deployment phase globally and has not yet formally entered India’s regulatory process. When it does, it will face versions of the same 100 percent foreign ownership concerns that are currently gridlocking Starlink, without Starlink’s head start on documentation, local partnerships, or political relationship-building in India.

The Kuiper question matters because it shapes the long-term competitive dynamics of India’s satellite broadband market as it matures. A market that clears OneWeb and Jio-SES first, lets Starlink eventually resolve its FDI issues, and then must process a third 100 percent foreign LEO operator will, by that point, have developed a much more settled, and likely more demanding, regulatory framework. Kuiper will enter a market shaped by its absence. That may be the most expensive consequence of Amazon’s slower commercial timeline.

Who launches first, and why it matters

The satellite broadband market in India is not winner-takes-all, the addressable opportunity is large enough to sustain multiple operators across different segments. But first-mover advantage in key verticals will be real and durable. Enterprise connectivity, government and defence applications, aviation and maritime, and institutional rural broadband (education, healthcare, banking) all represent early-revenue categories that whoever enters first will begin locking up through long-term contracts and infrastructure investment.

If OneWeb and Jio-SES are cleared ahead of Starlink, as the current trajectory suggests is likely, they will have a runway of 12 to 18 months to establish commercial relationships, build ground infrastructure, and develop customer inertia that makes switching costly. When Starlink eventually launches, it will offer a superior consumer proposition: its terminal hardware is simpler, cheaper, and easier to self-install than most VSAT alternatives. But it will be entering a market where enterprise relationships are already forming and where institutional procurement cycles are mid-stream. The consumer rural broadband segment, Starlink’s natural stronghold, remains open, but it is also the segment most dependent on clarity in the spectrum framework and device import logistics, both of which add lead time.

The question no approval decision will fully resolve

The deeper issue that India’s satellite broadband standoff surfaces is one that extends well beyond any of the individual companies involved: what governance framework applies to satellite operators whose physical infrastructure is in orbit but whose users are in India? LISL technology makes this question urgent because it enables routing architectures that are genuinely transnational in ways that terrestrial networks and even traditional geostationary satellites are not. Data can move between satellites in space before ever touching a ground station, which means it can move outside the jurisdictional reach of any single country’s regulatory enforcement before the regulator even knows it has left.

India is not wrong to ask this question. It is arguably among the first major markets to ask it seriously, at the level of pre-approval conditions rather than post-incident legislation. The delays are real, the costs to operators are mounting, and the opportunity cost to Indian consumers, particularly in underserved rural areas, is growing. But the questions being posed are not unreasonable. They are, in most respects, the right questions.

The challenge for India’s policymakers is to answer them without turning regulatory caution into regulatory paralysis. A government that uses security concerns as a legitimate instrument of governance is credible. A government that uses them indefinitely as a holding mechanism, without ever specifying what compliance would look like, risks being read, by operators and investors, as a market with an unpriceable regulatory risk premium. India’s satellite broadband aspirations and its broader digital connectivity ambitions are too important for that reading to take hold.

BCS Bureau