Trends

Western Europe: How can pay TV channels offset the decline in affiliate revenues?

Disney closing most of its channels in Western Europe and Sony Pictures selling its UK and CEE operations are two examples illustrating the diversion of traditional TV players away from linear and towards other forms of distribution, including in particular the launch of direct-to-consumer OTT services. But is this the only way forward for linear TV networks? What growth evolutions can be expected for these TV players?

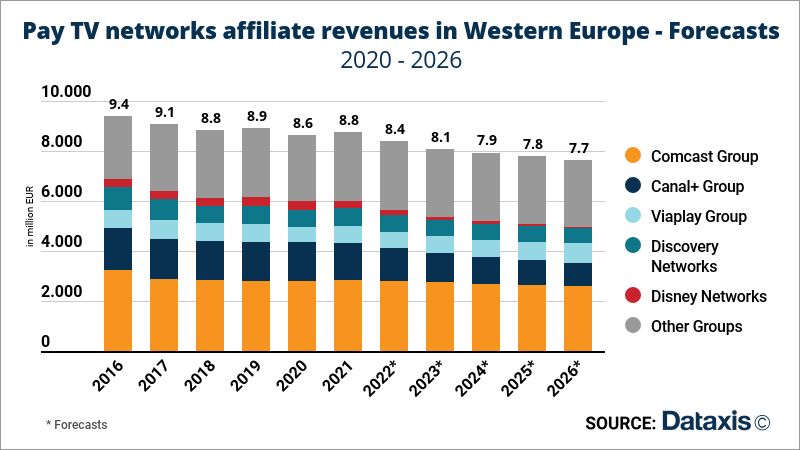

Affiliate revenues, which are the main source of revenue for paid channels, are expected to drop by 12% between 2021 and 2026. Current changes in consumption habits are pushing users towards more flexible content offers, particularly developed on OTT. An increasing number of users are consequently switching off their traditional pay TV standalone subscriptions (cable, terrestrial, satellite) and reducing the amount spent on TV services. The current state of the content distribution market is therefore putting pressure on telecom operators’ revenues, rising tensions in affiliate fees negotiations with pay channels, as shown during the dispute between Discovery and Sky in the UK and Germany, when Discovery’s channels were almost removed from the Sky network because of carriage fees disagreements.

While TV revenues in general are shrinking, the costs of audiovisual content production and acquisition are experiencing an inflationary trend due to streaming pure players’ massive investments rising the competition and the tough year the industry went through under covid restrictions – both financially and operationally. In this market environment, content creators are looking for other sources of revenue, often by taking advantage of the rise of OTT.

Indeed, OTT allows TV networks to free themselves from operators’ networks, save on distribution fees and create a direct source of revenue. It allows greater flexibility in content distribution to match users’ consumption patterns, alongside the development of more direct relationships with them. Besides, OTT facilitates international expansion since distribution doesn’t rely on operators’ fixed networks. The most striking example here is the Viaplay Group which was originally offering pay TV channels in Scandinavian countries, and is now present in 5 more countries with plans to make its platform available in 16 countries overall by 2023. Pay channels are turning more and more towards D2C distribution models. This strategy is also deployed by US majors with the launch of Disney+, and more recently the rollout of Discovery+ and Paramount+ in Europe. However, it comes with a cost, since it’s now up to them to acquire users and develop their own distribution service.

If affiliate fees are still a substantial source of income for TV networks, it will decrease in the future – as illustrated by Canal+’s 37% estimated decrease in affiliate revenues between 2021 and 2026, which translates the new strategic orientation of the group towards its OTT platform MyCanal. The estimated revenues generated through the platform should even offset the Group’s losses in affiliate revenues in Western Europe.

But whereas traditional live television has been losing attractivity in the eyes of Western European audiences, linear consumption should not be put too quickly aside. Channels benefit from a strong editorial expertise and have started to develop appealing lean back experiences on OTT with FAST channels – an approach illustrated by ViacomCBS’s PlutoTV service launched in 2018 in Europe. FAST channels, and ad supported streaming offers in general, represent another opportunity for traditional content editors to capture digital advertising revenues at a time when digital advertising expenditures keep on progressing, often at the expense of broadcast advertising. In the UK, ITV’s overall advertising revenues increased by 24% in 2021, but digital advertising revenues were a main post covid recovery driver with a 41% increase .

In a market where actors have been relentlessly adapting their offers in recent years, the optimal business model, preserving content providers’ revenues while meeting customers’ demands for flexibility, could still undergo major transformations before achieving stability. Victor Galland, Analyst at Dataxis

You must be logged in to post a comment Login