BCS Stories

The great bifurcation: India’s broadcast industry splitting into two irreconcilable businesses

India’s broadcast and pay-tv industry enters the second half of 2026 as two distinct businesses operating under the same regulatory umbrella, with little in common beyond a shared history. One is a legacy distribution chain accelerating structural decline, hemorrhaging subscribers at roughly a million per month, posting widening losses quarter after quarter, and shedding jobs across the field-intensive networks that once formed the backbone of television delivery in smaller cities and towns. The other is a capital-intensive, digital-first, rights-driven business that is growing rapidly, attracting fresh investment, and reshaping how India’s 969 million internet subscribers consume video.

This H1 2026 review examines both tracks with granular financial data, and asks whether the distance between them has become too wide to bridge.

The subscriber freefall: DTH in numbers

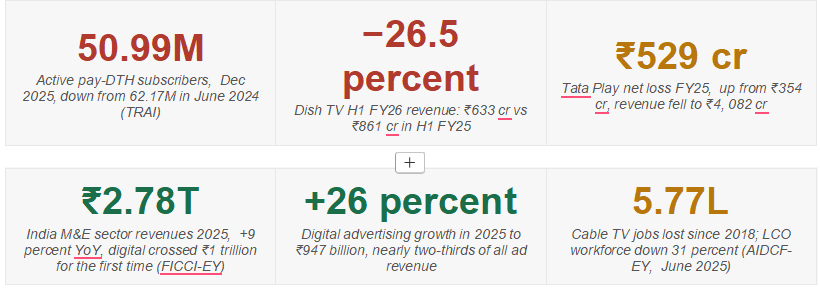

The TRAI data for H1 FY26 confirms what the industry has suspected for several quarters: the decline in pay-DTH subscriptions is not a plateau, it is an accelerating contraction. Active pay-DTH subscribers fell from 62.17 million in June 2024 to 56.92 million by March 2025, then to 52.78 million by September 2025, and to 50.99 million by December 2025. That is a net loss of 11.18 million active subscribers over 18 months, equivalent to losing the entire subscriber base of a mid-sized DTH operator every 6 months.

The pace of decline has, if anything, quickened. Between June and December 2025 alone, active pay-DTH subscriptions fell by 5.08 million, faster than the rate over the preceding twelve months. There is no seasonal or cyclical pattern that explains this. It is a structural trend driven by three simultaneous forces: affluent urban households migrating upward to OTT streaming; price-sensitive semi-urban and rural households migrating downward to DD Free Dish’s zero-subscription model; and a growing cohort of younger consumers who never enrolled in pay TV.

Market share within the shrinking DTH pie has also shifted. As of June 2025, Tata Play led with 31.42 percent of active users, followed by Airtel Digital TV at 29.33 percent, Sun Direct at 20.13 percent, and Dish TV at 19.13 percent. But Tata Play’s leadership comes amid an industry-wide subscriber decline, with no operator growing. The competitive question is no longer who gains share, it is who loses subscribers more slowly.

Operator financials: Losses deepen across the board

The subscriber trajectory maps directly onto operator financials, and the FY25 and H1 FY26 results make for grim reading across the board.

Tata Play, the sector’s largest operator, reported a net loss of ₹529 crore in FY25, up from ₹354 crore the previous year, a 49 percent widening in a single fiscal year. Revenue from operations fell 5.15 percent to ₹ 4,082 crore, with subscription revenue declining from ₹ 3,224 crore to ₹ 2,980 crore. For a business whose entire model is subscription-driven, a sustained fall in subscription revenue with no offsetting growth lever is structurally perilous.

Airtel Digital TV’s H1 FY26 results show a business that was marginally profitable 18 months ago has crossed into loss territory. Revenue for H1 FY26 was ₹ 1,516 crore, down from ₹ 1,535 crore in H1 FY25, a relatively modest 1.24 percent decline. But the profitability picture is sharper: Airtel Digital TV swung from a profit of ₹84.5 crore in H1 FY25 to a loss of ₹58.3 crore in H1 FY26, a ₹142.8 crore reversal in one year. Subscriber attrition continued through Q2 FY26, with the platform losing 3.4 lakh customers sequentially, bringing the total to 1.53 crore active users.

The most acute distress is at Dish TV, where the financial deterioration has moved from structural stress to acute crisis. H1 FY26 revenue collapsed to ₹633 crore from ₹861 crore in H1 FY25, a 26.5 percent decline over six months. Q4 FY26 results, released this month, showed a further 29 percent revenue plunge, signaling that the rate of decline is not stabilizing. Dish TV faces a compounding challenge: its subscriber base includes a disproportionate share of price-sensitive and rural customers most vulnerable to DD Free Dish migration, and it lacks Tata Play’s brand equity or Airtel’s ability to cross-subsidise through broadband bundling.

The DD Free Dish crossover: Free-to-air wins the scale war

One of the defining data milestones of H1 2026 is the effective convergence of DD Free Dish’s household reach with the total active pay-DTH subscriber base. With pay-DTH at 50.99 million by December 2025 and DD Free Dish estimated at 50–60 million homes across multiple industry surveys, the crossover point, where government-backed free television outscales all commercial pay platforms combined, has arrived.

The implications for the economics of the pay-TV ecosystem are severe. DD Free Dish operates on a fundamentally different financial model: broadcasters pay for slot allocation upfront rather than sharing subscription revenues, and consumers pay nothing. Every household that migrates to Free Dish permanently exits the subscription revenue pool. It stops contributing to MSO and LCO revenue streams, reduces the aggregate scale on which pay broadcasters negotiate carriage fees, and diminishes the advertiser reach premium that pay channels command over free alternatives.

For channels dependent on carriage fee income from pay platforms, particularly mid-tier general entertainment and regional language channels, the Free Dish migration represents an erosion of the economic base on which their content investment rests. The channels that remain on pay platforms are increasingly those that can justify premium subscription value: sports rights holders, premium English content providers, and top-tier Hindi GEC players. Everyone else faces a choice between accepting Free Dish economics or watching their distribution shrink.

The employment cost: 5.77 lakh jobs and counting

Behind the financial figures lies a human cost that aggregate market data does not fully capture. The AIDCF-EY State of Cable TV Distribution report, published in June 2025, based on responses from over 28,000 local cable operators across 34 states and union territories, estimated cumulative job losses in India’s cable TV sector at 5.77 lakh since 2018. LCO-level workforces have contracted by 31 percent, with the closures of approximately 900 MSOs and 72, 000 local cable operators accounting for a substantial share of the total.

These are not roles that convert readily to digital equivalents. Installation engineers, field service technicians, local advertising salespeople, and last-mile network operators are embedded in specific geographies, typically smaller cities and towns, where alternative employment in technology or media is limited. The jobs that replace them, in OTT platform operations, data analytics, and content delivery infrastructure, are concentrated in metropolitan centres and require skill profiles that take years to develop.

The employment contraction along the traditional distribution chain is, in a very direct sense, a transfer of economic value from distributed field-intensive employment to centralised technology employment. At the system level, value is being created. At the community level, in the tier-2 and tier-3 cities where most of India’s cable infrastructure operated, it is being extracted.

The digital track: Where the growth is going

The contrast with the digital and premium segments of the market could not be more pronounced. India’s overall media and entertainment sector grew 9 percent in 2025 to reach ₹2.78 trillion, according to the FICCI-EY annual report published in March 2026. Within that, digital media crossed ₹1 trillion in revenues for the first time, a landmark that underscores how decisively the centre of gravity in Indian media has shifted.

Digital advertising was the primary engine, growing 26 percent in 2025 to reach ₹947 billion, accounting for nearly two-thirds of India’s total advertising revenue. That proportion has continued to rise in H1 2026, as brands follow audiences onto connected screens and as measurable, targetable digital inventory increasingly displaces the broad-reach linear TV buy. For broadcasters without strong OTT presences, this advertising reallocation is a permanent structural headwind, not a cyclical correction.

OTT subscription revenues are on a growth trajectory that is among the steepest globally. India’s OTT market is projected to grow at a CAGR of 14.9 percent, the highest among the top-15 economies, reaching ₹ 35,061 crore by FY28. The platform consolidation accelerated in 2024, with the Reliance-Disney JV combining JioCinema and Disney+ Hotstar into a single entity with dominant rights across cricket, English sports, and premium entertainment. That merger created an entity with a subscriber base, content library, and distribution infrastructure that rival any streaming platform globally in terms of domestic reach.

For the remaining broadcasters and platform operators, the competitive landscape of H1 2026 is defined by the imperative to secure premium live content rights, the one category of programming that sustains linear viewing and supports both subscription and advertising monetisation simultaneously. This is the strategic logic behind Zee Entertainment’s June 2026 announcement of rights to 39 FIFA events through 2034, including the World Cups of 2026 and 2030 and the Women’s World Cup 2027. Reports suggest FIFA initially sought approximately $100 million for the tournament rights before settling at around $60 million, still a substantial commitment for a broadcaster that must monetise across both linear broadcast and Zee5’s streaming platform.

The regulatory backdrop: Ratings policy and measurement in flux

The regulatory environment has added a further layer of uncertainty to an already stressed broadcast landscape. The Ministry of Information and Broadcasting notified the Television Rating Policy 2026 in March, replacing guidelines that had been in place since 2014. The new framework mandates technology-neutral measurement, captures viewership across cable, DTH, OTT, and connected TV, and allows distribution platforms and OTT services to publish their own periodic viewership data without separate regulatory approval.

The practical effect of this change is significant. By enabling platforms to release viewership data independently, the policy makes the relative performance of linear versus digital consumption visible to advertisers in real time, with no filtering through a single measurement body. This transparency accelerates the advertising migration already underway: brands now have direct data to justify shifting budgets from linear TV to digital video, rather than relying on aggregated panel data that historically understated OTT viewership.

BARC itself faces a transition period of uncertain duration. The new policy requires the ratings agency to expand its measurement panel substantially, to 80,000 homes within six months and to 120,000 progressively, a compliance requirement that analysts have described as effectively pausing BARC’s current operational model until the expanded panel is in place. The temporary absence of credible, updated linear TV audience data creates its own market distortion, introducing uncertainty into advertiser planning cycles precisely when broadcasters most need stable measurement to defend their rate cards.

Outlook: Two businesses, one industry, and an unresolved policy dilemma

India’s broadcast industry in mid-2026 presents policymakers and investors with a structural challenge that cannot be resolved by regulatory adjustment alone. The legacy distribution chain, cable MSOs, pay-DTH operators, and the local operator networks that serve smaller markets are in secular decline. No tariff order revision, carriage fee adjustment, or subscriber incentive program has halted the erosion. The forces driving it, free-to-air alternatives, OTT substitution, and the economics of smartphone-plus-broadband, operate at a level that regulation cannot easily reach.

The digital and premium rights segment, by contrast, is growing at a pace that makes it one of the most dynamic media markets globally. India’s 969 million internet subscribers, rising ARPU on telecom plans, and the country’s demonstrated appetite for live sports and premium entertainment create a large, expanding total addressable market. The FICCI-EY projection of ₹3.3 trillion in total M&E revenues by 2028 is built on this digital growth engine, not on linear recovery.

The gap between the two tracks will not close; it will widen. The question for H2 2026 and beyond is how fast the traditional chain contracts, whether consolidation among DTH operators can generate the scale economics to slow the cash outflow, and whether broadcasters like Zee can execute hybrid linear-digital monetisation strategies fast enough to justify their rights investments before the linear revenue base that underpins them erodes further.

For every metric that matters to investors, subscriber counts, revenue trajectories, EBITDA margins, and loss ratios, India’s pay-TV sector is moving in one direction. For every metric that matters to the digital economy, advertising share, streaming revenues, OTT growth rates, and digital subscription penetration, it is moving in the opposite direction. The broadcast industry of 2030 will look very different from the one entering the second half of 2026. The only real question is whether the transition happens on terms that the industry controls or on terms that the market imposes.