Headlines Of The Day

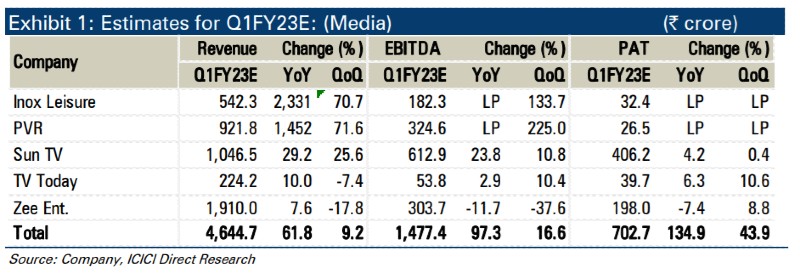

Result Preview – Media: Strong quarter for multiplexes!

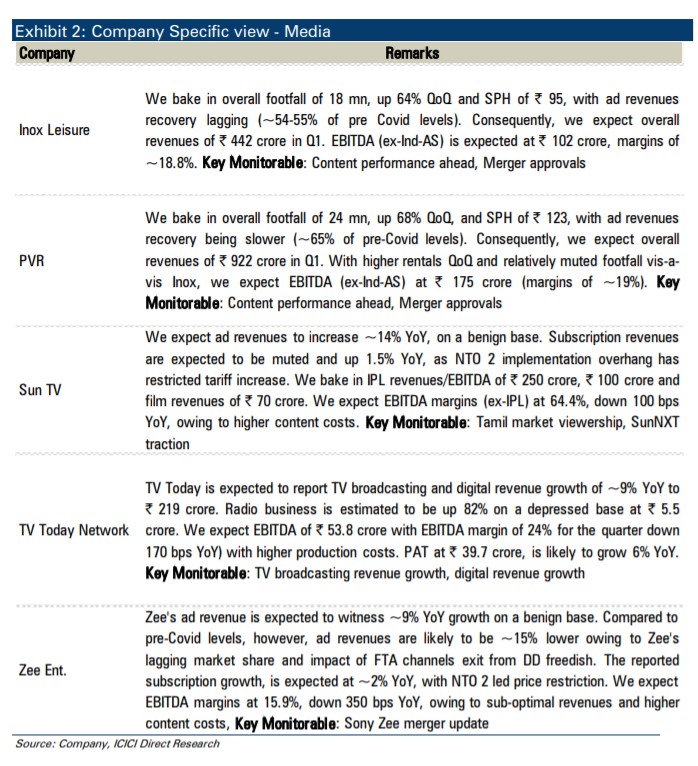

For multiplexes, strong box office collections of movies such as KGF 2, Bhool Bhulaiyaa 2, etc, is expected to result in a robust performance on topline and profitability front. For

broadcasters, while ad growth will be seen on benign base, margins will be lower amid higher content costs.

Multiplex: Strong box office collections to boost performance

The top contributor to collections were KGF 2 (~| 435 crore – Hindi), Bhool Bhulaiyaa 2 (~| 185 crore), Doctor Strange (| 127 crore) and RRR (residual collections during April). Furthermore, Vikram (in Tamil) did stupendous business. Thus, we expect net box office collections in Q1FY22 to be largely similar to pre Covid (Q1FY20) with strong movies such as Avengers: Endgame, Kabir Singh, Bharat, De De Pyar De like hits in the base. In terms of Q1 performance, we expect footfalls at ~18 mn and ~24 mn for Inox and PVR, up ~64% QOQ and 68% QoQ, respectively. We expect spends per head (SPH) for food and beverage for multiplexes to remain robust with Inox and PVR expected to report SPH of | 95, | 123, respectively. Ad revenues, however, would be lower at 55-60% of pre-Covid levels. We estimate EBITDA (ex-Ind-AS) of | 175 crore for PVR (margins of 19%) while bake in EBITDA (ex-Ind-AS) of | 102 crore for Inox (~18.8% margins). We highlight that coupled with strong topline performance, relatively lower than pre-Covid costs, will boost the margins during Q1. With strong content line-up in H2CY22, we expect strong collection momentum to continue and believe pre-Covid run rate will be attained quicker than anticipated.

Broadcasters: Mixed bag…

Q1FY23 is again expected to reflect a divergent performance among broadcasters with Zee relatively underperforming in ad growth amid impact of free to Airt (FTA) channel pullout from DD Free Dish. Sun TV’s ad revenues are likely to witness growth of 14% YoY, on a benign base. Subscription revenues are expected to be muted (up 1.5% YoY) amid NTO 2 implementation led pricing restrictions. We expect EBITDA margins at 58.6%, down 150 bps YoY, due to higher content cost. Zee ad revenue is expected to witness ~9% YoY growth on a benign base with lower growth owing to loss of ad revenues as it pulled out its GEC channels from DD FreeDish. The reported subscription growth, is expected to be muted at ~2% YoY. We expect margins at 15.9%, down 350 bps YoY, given the higher content costs and muted topline show. For TV Today, we expect ~9% YoY growth in TV and digital revenues. EBITDA margins at 24% are expected to be down 170 bps YoY, with higher production costs. PAT at | 39.7 crore, is likely to grow 6% YoY.

ICICI Securities