BCS Stories

JAS 2022, a weak quarter for the box office collections

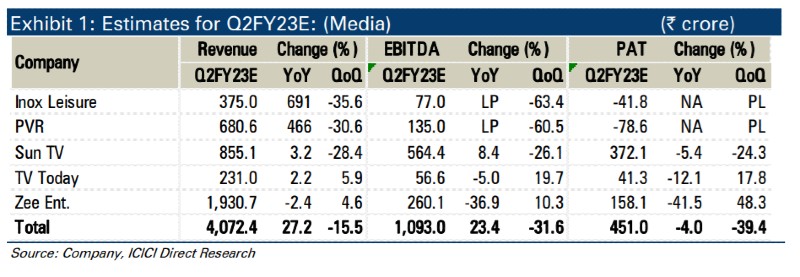

Weak quarter!

For multiplexes, weak box office collections of major movies are expected to result in a sharp decline in topline and marginal losses on the EBITDA front. For broadcasters, Q2 is anticipated to be a weak quarter on ad front.

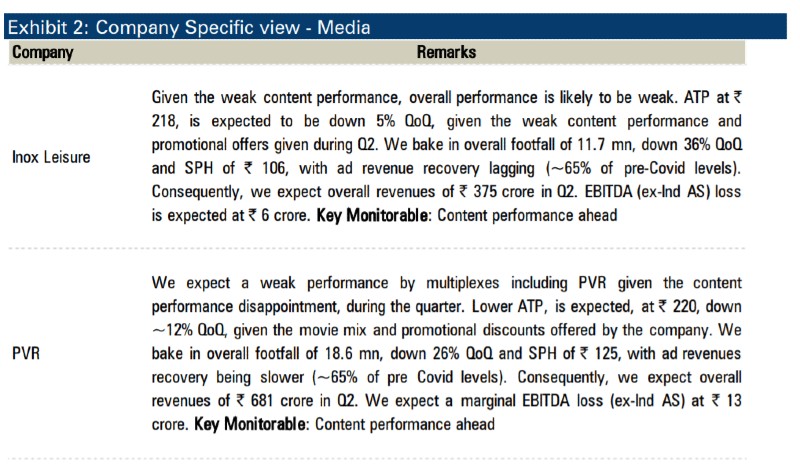

Multiplex: Flop show during quarter!

Q2 was a weak quarter with major big budget/starrer movies such as Lal Singh Chaddha, Raksha Bandhan, Shamshera, Liger etc, turning flop. Given the weak movies collection with only two movies (Brahmastra and Thor) crossing | 100 crore during the quarter, multiplexes are expected to witness —35-40% QoQ decline in box office revenues with weak footfall (down 26-36% QoQ) and average ticket price (ATP) decline ranging from 5- 12% QoQ for Inox and PVR. PVR, is expected to relatively witness less decline of —26% QoQ in footfall, aided by south movies footfall, albeit same will result in lower ATP at | 220, down —12% QoQ, given the movie mix and promotional discounts offered by the company. Advertisement remains at —65% of pre Covid for both multiplexes. We expect both PVR and Inox to report marginal EBITDA losses (ex-Ind-AS) given the weak content performance. With a strong content line-up in H2FY22, we expect strong collection momentum to return from Q3.

Broadcasters: Ad weakness likely!

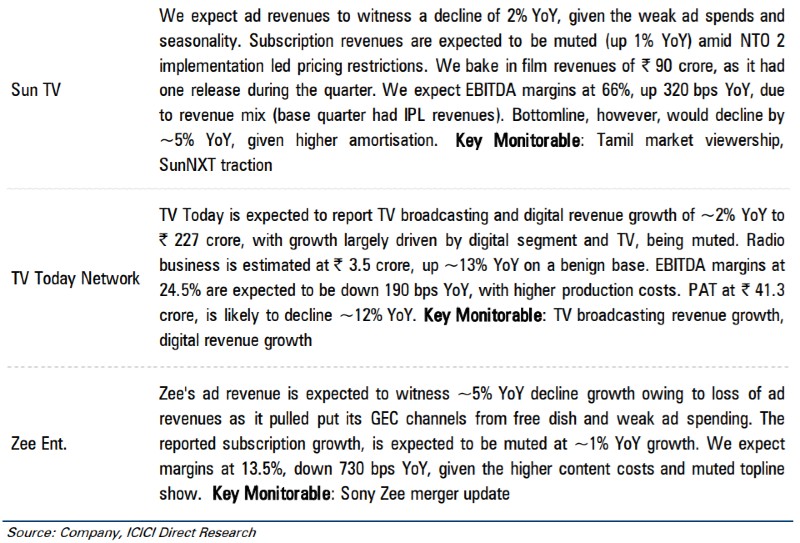

During Q2FY23, GEC broadcasters are expected to witness a weak quarter with low to mid-single digit YoY ad decline owing to a) exit of free to air channel by Zee; b) weak ad spending in July, August and c) overall weak seasonality.

Sun TV’s ad revenues is likely to witness decline of 2% YoY, given the weak ad spends and seasonality. Subscription revenues are expected to be muted (up 1% YoY) amid NTO 2 implementation led pricing restrictions. We expect EBITDA margins at 66%, up 320 bps YoY, due to revenue mix (base quarter had IPL revenues). Bottomline, however, is expected to fall —5% YoY, given higher amortisation. Zee ad revenue is expected to witness —5% YoY decline growth owing to loss of ad revenues as it pulled its GEC channels from free dish and weak ad spending. The reported subscription growth is expected to be muted at —1% YoY growth. We expect margins at 13.5%, down 730 bps YoY, given the higher content costs and muted topline show. For TV Today, we expect —2% YoY growth in TV and digital revenues, with growth largely driven by digital segment and TV, being muted. EBITDA margins at 24.5% are expected to be down 190 bps YoY, with higher production costs. PAT, at | 41.3 crore, is likely to decline —12% YoY.

Going ahead, we expect an ad revenue recovery from Q3 onwards led by festive spends. The ad recovery would also bring in a margin improvement for broadcasters, going ahead.

ICICI Securities