Reports

COVID-19 – The many shades of a crisis

The COVID-19 pandemic is unique in that it is has not only led to considerable loss of human life, but also widespread economic hardship through concurrent supply (input constraints), demand (spending patterns, consumer confidence), and market (financial conditions impacting wealth) shocks. India’s real GDP growth had already decelerated to its lowest in over 6 years at 4.7 percent in 3QFY20. The COVID-19 pandemic, resultant lockdown, and social distancing measures can only be expected to worsen prospects across manufacturing and services. Along with lower consumption levels and higher unemployment, the Indian economy is likely to face a particularly challenging time in the months ahead.

An M&E sector perspective

The media and entertainment (M&E) sector in India was estimated at `1631 billion in FY19 and grew at a CAGR of 11.5 percent over the 5-year period FY15–19. This was against an overall rate of growth in the country’s GDP at 7.2 percent during the same time. Typically, media consumption has tended to be income-inelastic. However, the current environment is unprecedented, and could result in a dip in media consumption in the near term and importantly, a realignment in consumption models. During the lockdown, however, certain segments of M&E are seeing consumption growth, particularly in TV, digital, and OTT. Further, most segments (except news-related businesses) are unable to offer new content with production stalling across formats. Monetization in the M&E sector is predominantly reliant on advertising, which has seen a major contraction. Overall ad-spend is determined by the performance of sectors such as FMCG, e-commerce, automotive, financial services, and real estate, all of which currently face their own challenges and could, therefore, take time to recover.

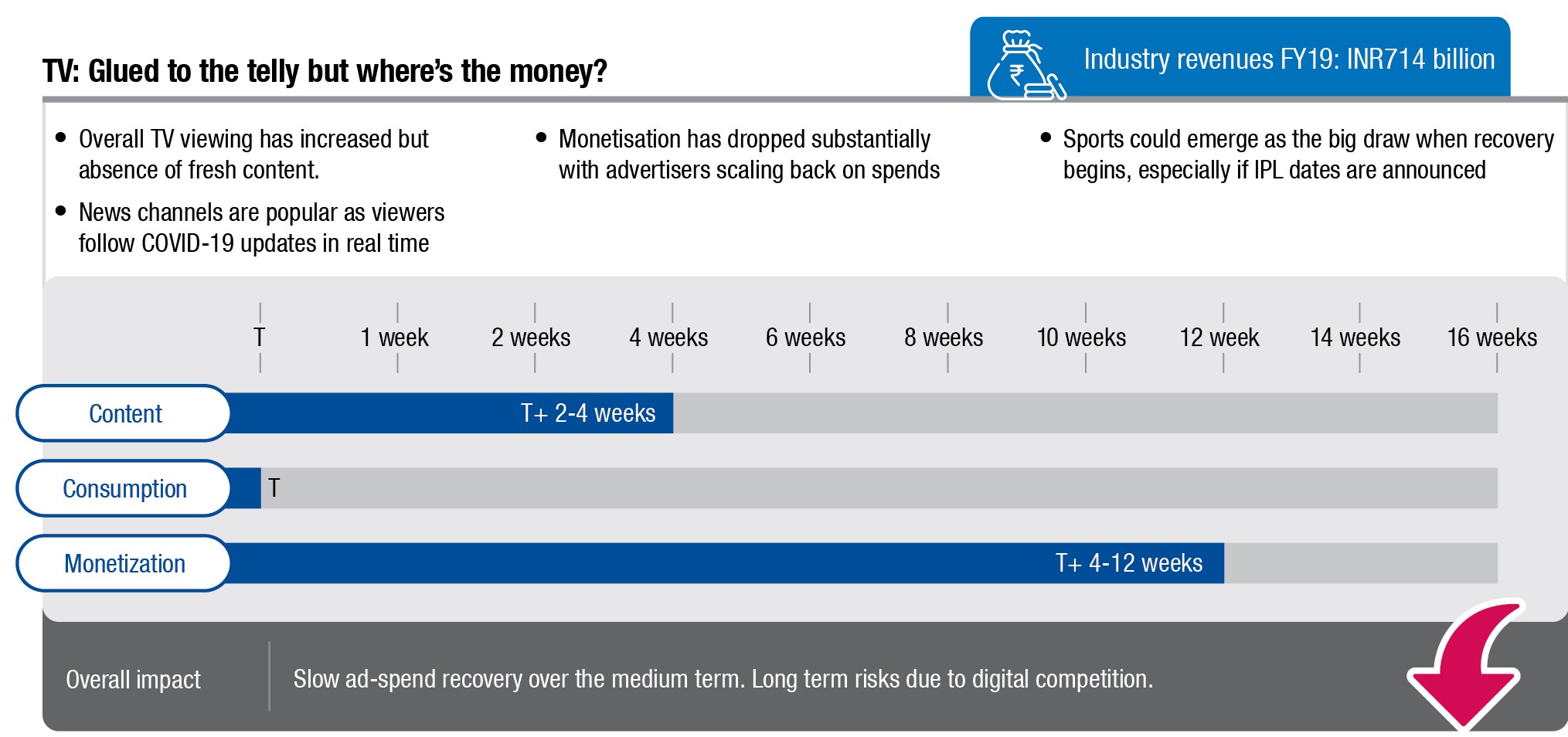

TV – Glued to the telly but where is the money?

Overall TV viewing has increased but there is an absence of fresh content. News channels have gained popularity as viewers follow COVID-19 updates in real time. Monetization has dropped substantially with advertisers scaling back on spends. Sports could emerge as the big draw when recovery begins, especially if IPL dates are announced.

A whole new world? Insights into the crisis and its aftermath

Ad-spend pressures are expected to linger on the back of weak economy and lower domestic consumption. At-home entertainment options (digital, TV) will see an upswing as lockdown behavior results in habit formation. There will be delayed expansion plans though digital businesses aggressively target market opportunity. These themes will play out across the M&E value chain.

Supply chain

Innovations in content pipeline. Limited content banks have severely constrained broadcasters and platforms. Current supply chains have limited remote-collaboration options, longer lead times, and a lack of technology integration. A focus on building a stronger content bank may result in working capital being locked up across the value chain, leading to higher cash flow requirements. Focus on technology integration, process efficiencies, and reduction of lead times. Aspects such as remote collaboration for creative ideation and scripting could last well beyond COVID-19, and alter forever the way the industry creates content.

Cloud solutions and remote working. With greater harnessing of cloud and remote-working solutions, companies may look at efficiencies in the way they conduct business, even across revenue-generating functions such as sales.

Innovations in delivery models. With outdoor entertainment and recreation facing challenges in the near term, innovative outreach, and delivery models are likely to evolve. Virtual live events and film exhibitors could be expected to leverage technology to reach consumers directly.

Greater emphasis on predictive analytics. Companies could place an increasing amount of reliance on AI/ML to predict consumer behavior in these uncertain times.

And finally, cash is king. There is likely to be near-term focus on sustenance at current levels by companies. There may be a drastic fall in the CapEx/investment cycle by companies, which could constrain supply and the growth of the M&E industry in the near term.

Monetization

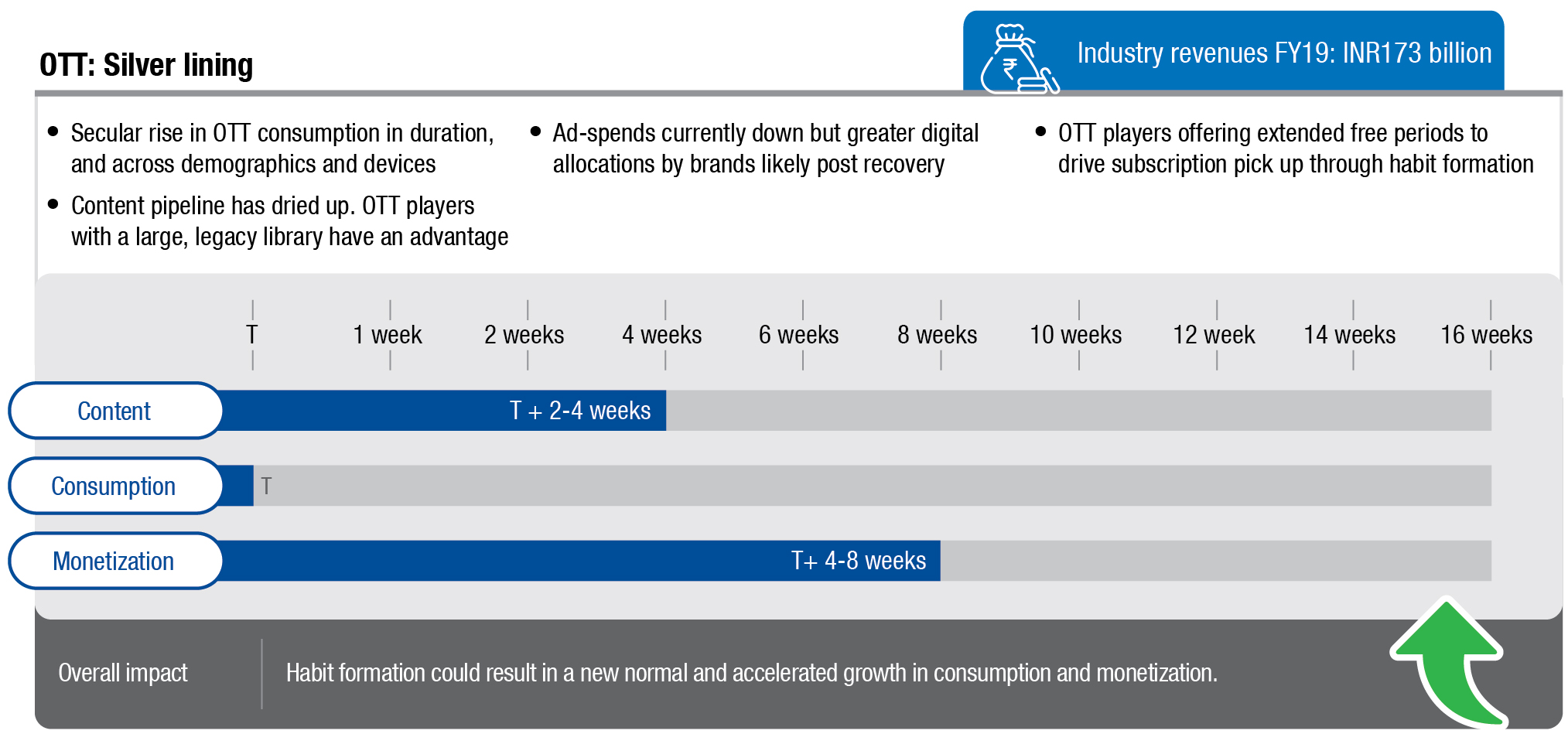

Longer timelines for ad spend recovery. An economy under stress, and the adverse impact on the key ad-spend sectors, is likely to impact monetization significantly. As a result, though consumption may rebound earlier, monetization recovery may take longer. Penetration of subscription-based digital models will accelerate. Digital consumption has been one of the beneficiaries of the lockdown, though advertising-led monetization is not going to be immune to the overall cuts in advertising. However, digital-subscription revenues could see an upswing post COVID-19 as habit formation in terms of OTT video consumption sets in. Currently, though subscription monetization is low since most platforms are offering free trials and sign ups to attract new audiences, with potentially higher paid conversions subsequently.

React to cope, respond to thrive

The economic recovery can be expected to present its fair share of complexities, as organizations respond to pressures on multiple fronts. With a hard reset for a number of businesses, all aspects of operations would need urgent attention. Organizations might need to be risk-focused and innovate existing business models and processes to survive and emerge stronger.

Technology takes center stage. Digitization and building strong integrated digital models will become essential rather than optional in the post-COVID era. For digital companies, increased focus is required on strengthening technology backbone, as digital penetration is expected to become more widespread once normalcy is regained. Digital-media consumption provides the opportunity to build faster and more nuanced profiles of users. The trend of using technology to enhance customer engagement – recommendation engines, personalization, feedback loops, data analytics – will only accelerate and deepen. Apprehensions around individual privacy online could become stronger and companies can expect to face a backlash should they not have credible measures in place for data protection.

Building supply chain resilience. Emphasis on deepening content pipeline, building content banks, and reducing lead times. By leveraging technology and its associated tools – telecommuting, cloud, AI/ML – M&E companies should invest in improving content-output efficiencies. Enable recommendation engines to showcase less explored parts of content library, gamification of content, when production is hampered in exigencies.

Cash regains supremacy. Trend of risk aversion is not just for consumers, but also for organizations as liquidity allows for a great degree of comfort and confidence during stressful times. Media spend by companies across sectors might be subject to a higher level of scrutiny and, therefore, M&E companies might need to offer more accurate return on investment calculations in traditional media and greater programmatic advertising options on digital platforms. M&E companies might be more inclined to review the cost of acquisition (CAC) of new users, resulting in some downward pressure. CapEx and expansion plans would need to be reassessed to balance cash requirements, growth ambitions, and consumption dynamics.

Lowering operating leverage. Emphasis on flexibility as companies look to move to a variable cost model and reduce fixed costs. As this crisis has shown, the ability to remain agile during downturns is a valuable asset. Most content producers are paid ahead to allow them to manage their own working capital, but such upfront contractual payments could be re-negotiated to avoid locking up cash.

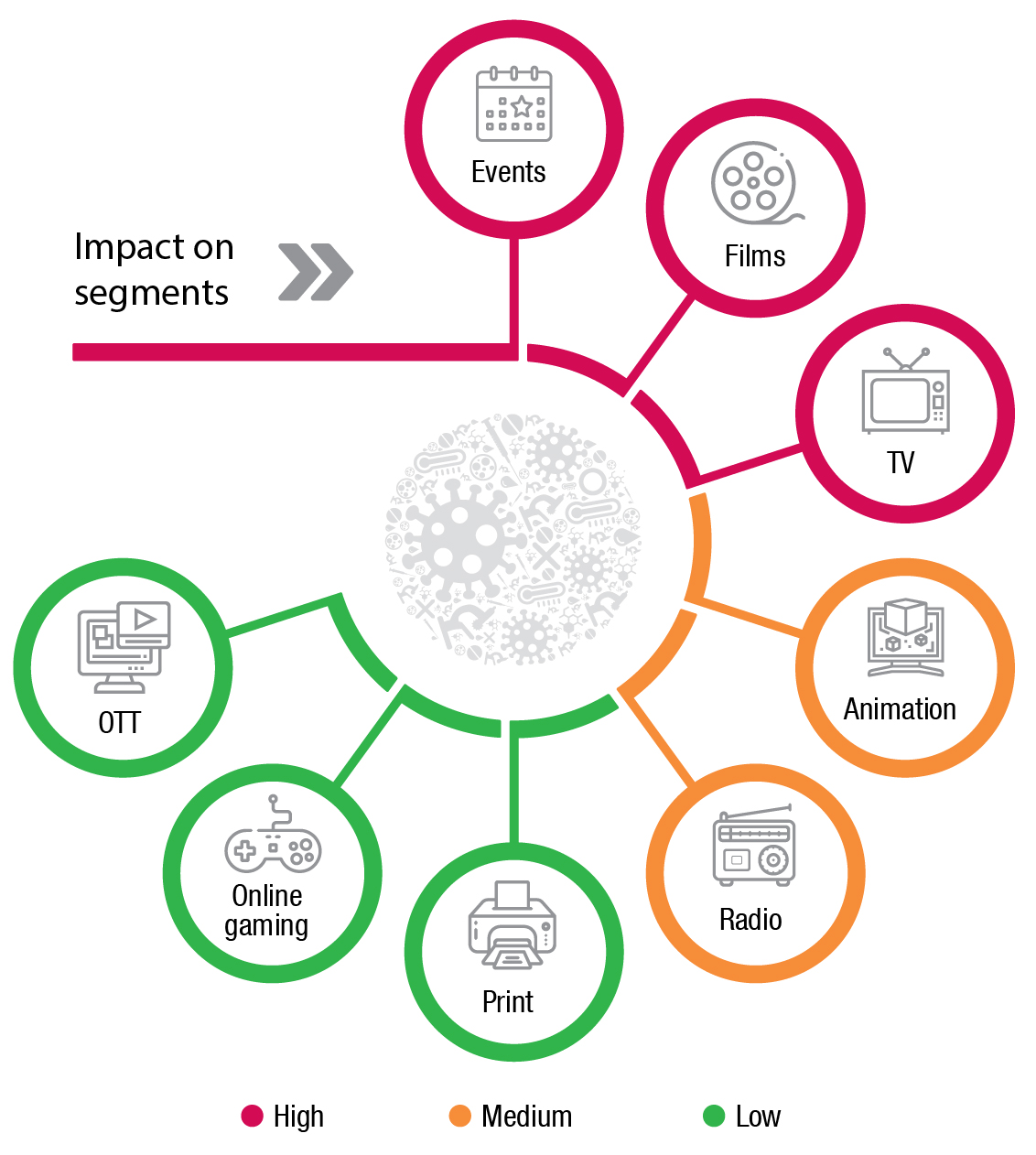

While traditional media could face some challenges in the near to medium term, digital media businesses have fared relatively better, albeit only on the consumption side. There is likely to be a long-term – upward – shift in the integration of digital technologies into our everyday lives, and media and entertainment will be an immediate beneficiary. This is likely to be true across socio-economic groups – i.e., for both India and Bharat.

The differences could arise, however, with a more granular observation of individual behavior, as we expect urban areas affected by COVID-19 to potentially show greater affinity for at-home entertainment, subscription content, cord-shaving, and streaming to larger screens in the near to medium term. On the other hand, livelihoods of a large segment of Bharat have been severely affected by this pandemic, potentially making entertainment spends into an aspiration. Inequity and imbalance in consumption could even be exacerbated in our post-crisis reality.

So, while a quick recovery is hoped for, and everyone looks forward to putting the pieces of their lives back together over the next few months, much would have changed in the world. Entertainment across all its forms could provide some much-needed succor.

Experts speak

Satya Easwaran

Satya Easwaran

Partner and Leader,Markets Enablement, TMT,KPMG in India COVID-19 pandemic began at a time of increasing global economic vulnerability. There were already genuine concerns of falling consumption levels and investment alongside rising unemployment. Brexit and the US-China trade war had not helped and there was a palpable sense of uncertainty. Most indicators now suggest that some of the largest economies stand on the precipice of the greatest real recession in nearly 100 years. As far-fetched as it seems right now though, there will be a recovery and people are already asking: how different will the post-COVID-19 era be from the one we knew earlier? The most tangible effect we see is on technology adoption and general versatility with digital commerce and content. We anticipate a considerable acceleration on both fronts for individuals and businesses, which should hopefully do as much for financial inclusion and e-governance as for streaming services. There has been a perceptible increase in media consumption – TV, digital, and gaming especially – during the last few weeks as people have remained homebound.

Monetization of this trend could prove challenging, however, as the media and entertainment sector in India derives a majority of its revenues from the advertising spend of other industries. The recessionary impact on FMCG, financial services.

Girish Menon

Girish Menon

Partner and Leader, Media and Entertainment, KPMG in India

“The automotive, and e-commerce, therefore, could have a knock-on effect. On the other hand, subscription revenues for the sector could improve over the medium term, as people are exposed to and get accustomed to a greater variety of content during this lockdown period. This is predicated on new content being available quickly once the restrictions are lifted, which as per our analysis should correct with a lag of one to four weeks.

The segments most affected by the lockdown have been those that rely on a social gathering of people – films and events – and the recovery here might take longer than anticipated. Certain sections of consumers – particularly those residing in COVID-19 hotspots, for example – are likely to remain apprehensive of crowds and display a preference for at-home media and entertainment options over outdoor experiences.

More generally, there could be a shifting of priorities as we progress to a new normal; the balance between work and family, wealth and well-being might be re-evaluated with leisure – of which media and entertainment is a large part – playing a greater role in our lives.”

Based on COVID-19: The many shades of a crisis – A media and entertainment sector perspective, a report by KPMG.

You must be logged in to post a comment Login