Regular Column

Stakeholders express concern on TRAI’s consultation paper on tariff-related issues for broadcasting and cable services

The TRAI has recently issued a consultation paper on tariff-related issues for broadcasting and cable services, which covers different aspects related to the new tariff order (NTO), which came into force from February 1, 2019, and invited comments from stakeholders.

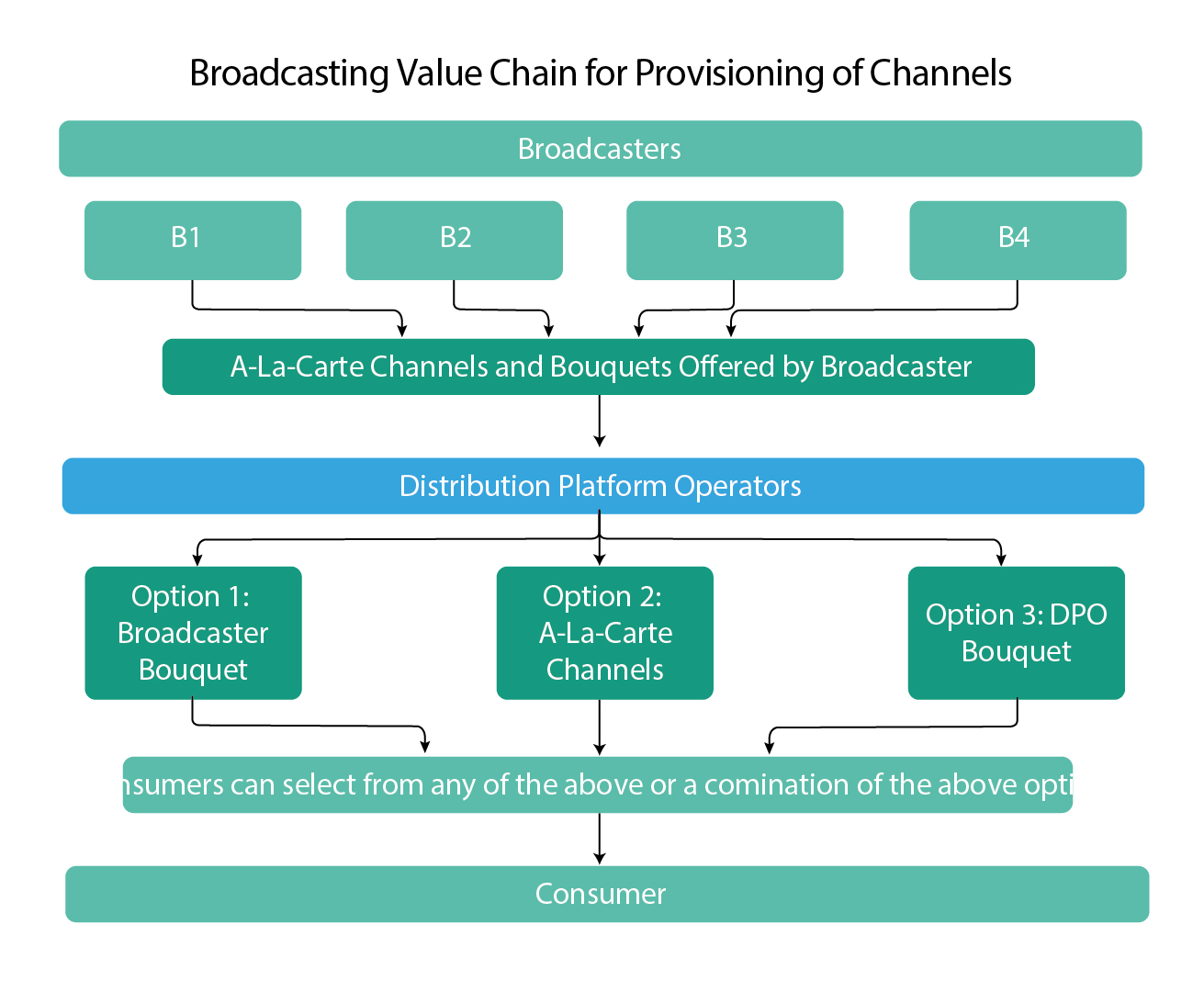

The three main issues that TRAI has sought to address with the consultation paper are – whether channel bouquets should be allowed; should a cap on discounts within bouquets be reintroduced; and whether the ceiling price of channels in bouquets – `19 at present – needs to be re-examined.

The concern expressed by broadcasters on this issue is that if TRAI disallows broadcasters and distribution platform operators (DPOs) – a term used for cable operators and DTH providers – from assembling bouquets, this will severely impact their business model as many smaller and less popular channels will not get enough audiences and lose reach and thus viewership, resulting in a further drop in advertising revenue, and perhaps finally exiting the business.

TRAI fixed `19 as the MRP cap for channels under the NTO. However, it has found that broadcasters have kept all the popular channels (66) in the top bracket. These consist mostly of Hindi and regional general entertainment channels and sports channels. Now, if the Authority re-examines the pricing, the channels may lose the power to reinvest in premium content, especially when they are facing tough competition from video-streaming services.

India Ratings and Research (Fitch Group) believes TRAI’s tariff and interconnection regulations will require six to eight more months for effective implementation due to challenges related to revenue sharing between multiple system operators (MSOs) and local cable operators (LCOs); treatment of long-term packs already sold by direct-to-home (DTH) players and repricing of channel bouquets.

However, the tariff order is likely to de-risk the business model of MSOs and LCOs as their revenue stream will contain fixed network-capacity charge (NCC) from subscribers and content commission from broadcasters (BC), thereby effectively passing through content cost. DTH players, on the other hand, could see their profitability being impacted in the next 6 to 12 months, since they have already sold long-term plans till end of 2018 and DTH companies would not be allowed to withdraw or re-price a plan that’s already in use.

Post TRAI’s removal of the 15-percent discount cap on bouquet price versus à la carte channel pricing, broadcasters have started offering bouquet of channels, at 20–60 percent discount to the a-la-carte channel pricing, presumably to avoid any hike in final consumer price. However, despite similar costs, consumers will have access to fewer channels compared to the previous tariff regime.

Broadcasters’ business model will change from B2B (selling content to distributors) to B2C (selling content to consumers) as broadcasters will now market their channel bouquet to end customers rather than rely on MSOs. Broadcasters with strong set of anchor channels across genres will benefit, as they will be able to create a comprehensive bundled offering and generate customer pull.

TRAI’s consultation paper primarily focused on making the existing order more end-user friendly. Certain aspects in the consultation paper, such as reinstating cap on discount provided on bouquet pricing, moderating/regulating the number of bouquets, as well as number of channels, may face operational and legal challenges during execution. Allowing a fixed discount on total prices of selected à la carte channels would empower end customers to choose their preferred channels (even across broadcasters) and also reduce their monthly payouts.

You must be logged in to post a comment Login