Cloud

Accelerated Consolidation Ahead

It has been roughly 70 years since cable TV first appeared and during that span of time, the pay-TV industry has survived lot of upheaval. But perhaps no bigger wave of disruption has ever hit the industry than the one crashing right now. The market’s established pay-TV providers are facing a range of new challenges from streaming video behemoths and upstart providers alike. And the number of new players entering the market – some carrying familiar names and others not – seems to be growing exponentially. Further, this turmoil is spilling into almost all sectors of the business, from advertising to distribution to the very screens consumers are using to watch video.

Market Dynamics

The global pay-TV market is valued at USD 247,000 million in 2018 and is projected to increase significantly at a CAGR of 2.7 percent from 2019 to 2028 by MarketWatch.

The market may be segmented into IPTV, satellite TV platform and cable and terrestrial TV platforms. Major global players include Comcast, Dish, Time Warner Cable, Verizon, Netflix, Bharti Airtel, CenturyLink, Deutsche Telecom, ARRIS Group, Cisco Systems, Broadcom Corporation, Ammino Corporation, MatrixStream Technologies, Orange S.A., and Eutelsat.

USA

The top pay-TV providers in the US representing close to 95 percent of the market have seen their percentage of lost subscribers double year-over-year for three consecutive years now, according to Leichtman Research Group. In 2018, pay-TV providers shed more than 3 percent of their subscriber base, nearly twice the percentage loss from 2017 (-1.6 percent).

Discounting internet-delivered services, such as Sling TV and DIRECTV NOW, which saw an increase of 19 percent in 2018 (compared to the 90 percent experienced in 2017), traditional pay-TV services lost more than 3.5 million subscribers last year. That is up from a contraction of 3.1 million subscribers in 2017.

Counting subscribers for internet-delivered services, the total pay-TV market shed roughly 2.9 million subscribers last year, almost double the number (~1.5 million) from 2017. The pace of cord-cutting continues to accelerate as the major subscribers churned fewer than 126,000 subscribers as recently as 2014.

- Again this year, all types of providers were hit hard, though some worse than others:

- The top telephone providers such as Verizon FiOS shed 2.6 percent of their video subscribers, although that was a better result than 2017 (-8.7 percent);

- The churn rate for the top satellite TV services was 7.5 percent, compared to a loss of 4.7 percent in 2017; and

The top cable companies lost 1.9 percent of their subscribers, up from their loss of 1.4 percent in 2017.

By contrast, Netflix had 58.5 million paying subscribers in the US as at the end of 2018, which was almost 11.5 million more than the top cable companies combined.

Also, the broadband subscriber market continues to expand. The top broadband companies representing 95 percent of the market added about 2.4 million net subscribers last year. Cable companies fared particularly well, with more than 2.9 million subscriber additions, while the top telecommunications companies lost almost 470,000 subscribers.

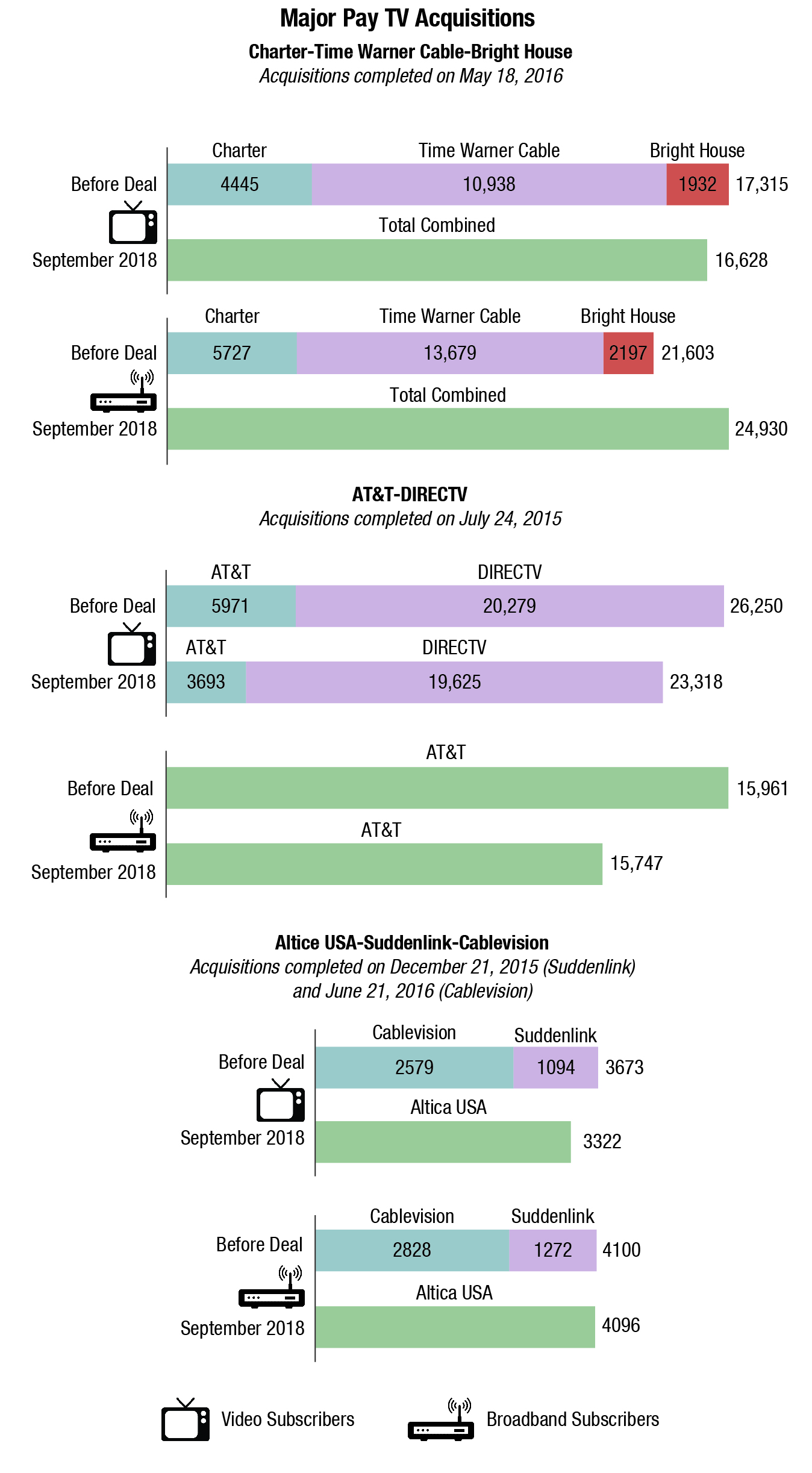

Moving ahead, the year 2019 promises to bring big changes for several of the biggest pay-TV providers in the US, especially for those that participated in the wave of M&A that swept over the industry in the last few years.

During that wave, the US pay-TV market saw a number of multibillion-dollar deals, including Charter Communications Inc.’s combination with Time Warner Cable Inc. and Bright House Networks LLC, Altice USA Inc.’s roll up of Suddenlink Communications and Cablevision Systems Corp., and AT&T Inc.’s acquisition of DirecTV Group Holdings LLC. All of these companies stand ready to enter a new phase in 2019 as they continue to transform themselves to compete in a changing video market.

Vivek Couto

Vivek Couto

Executive Director, Media Partners Asia

“Pay-TV stakeholders are adjusting to new realities as the industry shifts to IP-based distribution. The growth of high-speed broadband and online video is driving fundamental changes in content consumption and investment across key markets. This, together with piracy, will continue to adversely impact pay-TV industry’s growth. There will be more fixed broadband subs than pay-TV subs across much of Asia-Pacific by 2021. M&A activity for the Asia-Pacific broadcasting and pay-TV sectors for 2017 and the first half of 2018 reached USD 10.5 billion in aggregate, with the biggest deals taking place in Australia, India, and Korea. More M&A and consolidation is likely in these markets with Southeast Asia likely to join the action over 2019-20.”

The Asia-Pacific region

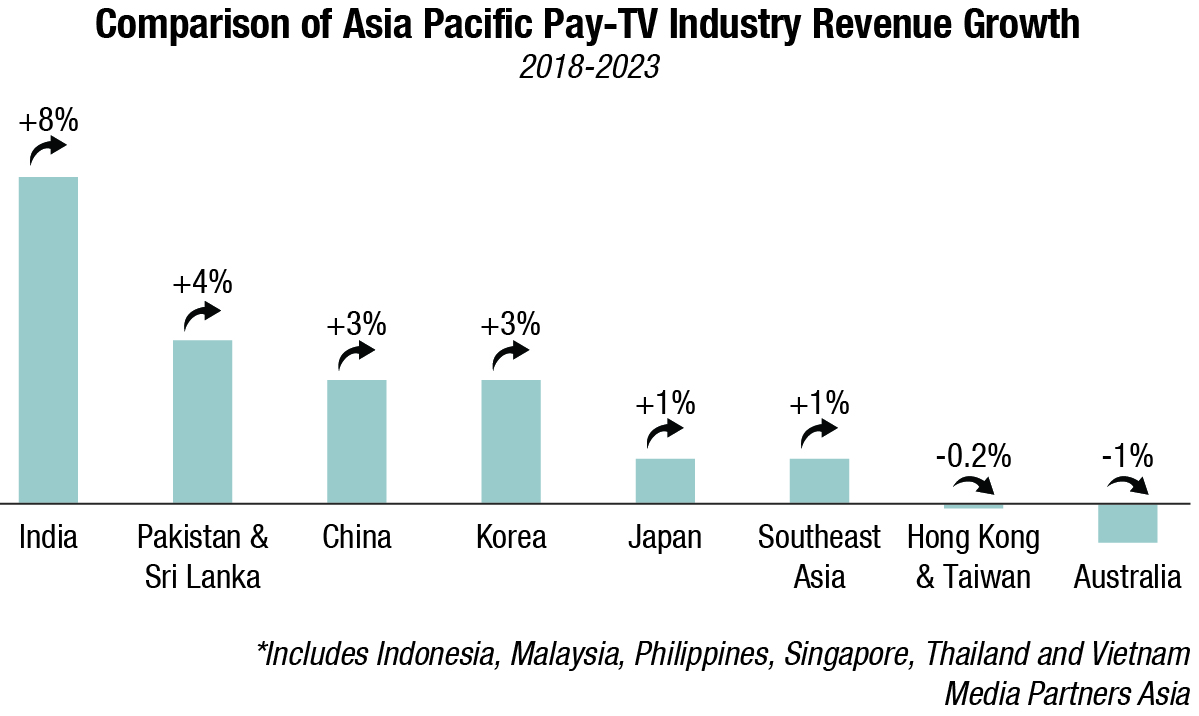

The APAC pay-TV revenue, which comprises of subscription fees and local and regional advertising sales, will expand at a 3-percent CAGR between 2018 and 2023 to exceed USD 66 billion in revenue by 2023. In 2018, the pay-TV revenue is projected to grow 5 percent to top USD 56 billion.

The Asia-Pacific region is looking at a phase of consolidation as subscriber growth and spend deteriorate across key territories, according to Media Partners Asia (MPA). Aggregate revenues across 13 major pay-TV networks in Asia-Pacific grew by just 1 percent in 2018 to reach USD 4.9 billion (following 5 percent growth in 2017), while combined EBITDA fell by 5 percent in 2018 to USD 0.9 billion, approximately the same rate of decline as 2018.

Over the next five years, the biggest gains will come from China, where pay-TV revenues are projected to grow at a 3-percent CAGR to reach USD 25 billion by 2023, and the more accessible and commercial India market, where pay-TV revenue is set for a whopping 8 percent CAGR to reach USD 16 billion by 2023. That makes India the highest growing and most scalable pay-TV market in Asia-Pacific. At the same time, South Korea will grow at a 3-percent CAGR to reach USD 7.4 billion in revenue by 2023, according to MPA forecasts, while pay-TV revenue in Japan will climb at a meager 1 percent CAGR to touch USD 7.1 billion over the same time-frame.

Elsewhere, pay-TV momentum will moderate in Indonesia and the Philippines, two of Southeast Asia’s biggest growth economies, according to MPA, while Australia, Hong Kong, New Zealand, Malaysia, Singapore, and Thailand will register revenue declines ranging between a -1 percent to a -6 percent CAGR over 2018–2023.

Consumer demand for traditional pay-TV has been impacted forever by high-speed broadband, which is driving rapid increases in online video consumption as well as piracy. These trends have intensified downward pressure across Asia’s pay-TV ecosystem, especially in South-East Asia, led by Singapore and Malaysia, alongside secular shifts in Australia and New Zealand, and are likely to accelerate consolidation as well as major shifts in how channels and content are marketed and sold. The first big wave of pay-TV consolidation has been led by Walt Disney buying 21st Century Fox and AT&T buying branded networks from Turner and HBO, which will play out with momentum across Asia-Pacific over the next year. Future consolidation and rationalization will be defined by global moves and M&A possibilities involving large assets in India. Major players such as Discovery, CBS, Viacom, A+E, Sony, and Universal are now competing for consumers’ attention along with Disney and a newly integrated WarnerMedia within AT&T.

Meanwhile, Asia’s relatively young online video market continues to expand rapidly, fuelled by advertising scale in particular. Online video revenues in Asia-Pacific grew 40 percent in 2018 to total USD 8 billion, according to MPA. As part of this, online video advertising grew 36 percent to reach more than USD 5 billion while subscription revenue grew 50 percent to surpass USD 2.8 billion. Outside China, Google (YouTube), Facebook, Netflix, and Amazon still dominate advertiser and wallet share, although local players are starting to emerge with scale, including Stan in Australia, Hotstar (now owned by Disney) in India, Hulu in Japan and Viu in Hong Kong and Southeast Asia.

Pay-TV and telecom operators are also increasingly investing in platforms and technology to aggregate OTT (over-the-top) services and provide more choice to their customers along with simpler packages of pay channels with digital rights. In India, the major telecom players, like Reliance Jio and Bharti Airtel, have tied up with streaming services like Amazon Prime Video, Eros Now, and others for their content to be available on their platforms.

Tata Sky and Dish TV India are two of the world’s biggest success stories when it comes to global satellite pay-TV over the last few years.

Harit Nagpal

Harit Nagpal

CEO, Tata Sky

“There are 50 million DTH Households, 100 million cable TV households and 100 million homes without a TV in India. There are opportunities to convert cable to DTH, and to get these new households, we will look to upsell existing customers to higher packages. We have enough room to grow.”

Way forward

The operators who will be most successful in the future are those aggregating multiple types of content from a wide range of sources, making it available to subscribers in an easy and attractive way from a unified UI. Today, the television experience is much too fragmented, with viewers having many different services to choose from.

Operators can solve the issue of viewer fatigue, and be the prime source of home entertainment by making all of those offerings accessible in one place with simple navigation and personalised content recommendations. Optimizing and even extending data capturing into the client middleware and the app of user activities will be key to supporting operators maintain a profitable business and provide subscribers with easy search to find the type of content that they desire.

Anil Dua

Anil Dua

Group CEO, Dish TV India

“I do not see OTT as a threat to the satellite industry. Television is an irreplaceable part of the Indian household as it serves four to six family members while promoting family leisure time. Content over apps is individually consumed and is, therefore, supplementing family TV viewing. Not only is DTH pricing considerably lower when you compare it to OTT, but it also offers a wide variety of content in multiple languages, thereby catering to consumers of all ages, geographies, gender, communities, etc. Going forward, we would like to see non-TV households coming into the fold and also digitization picking up the pace. The viewership for linear channels and online video consumption will both coexist.”

You must be logged in to post a comment Login